/ Conferences

World Hydrogen Asia

July 8 - 10, 2025 | Tokyo, Japan

/ Conferences

/ Conferences

July 8 - 10, 2025 | Tokyo, Japan

/ Conferences

Join Eduard Sala de Vedruna, Shankari Srinivasan and Catherine Robinson at World Hydrogen Week as they delve into the key insights and developments from the conference. Discover the pace of project advancements, with discussions highlighting both positive momentum and some slower-than-expected progress. Learn about the evolving role of consumers and the ongoing discussions around offtake agreements, especially in Europe.World Hydrogen Week, organized by World Hydrogen Leaders as part of SP Global Commodity Insights, brings together industry leaders for in-depth discussions on the latest technologies and market dynamics. Stay tuned for more updates as we explore the interplay between natural gas, LNG, and hydrogen, shedding light on the critical links that will shape the future of the hydrogen economy.

Dive into the future of hydrogen at World Hydrogen Week in Copenhagen!Join Matthew Hodgkinson and the SP Global hydrogen analytics team as they explore the latest advancements in the industry, including cutting-edge technologies like solid oxide electrolysis. Gain insights into the challenges that lie ahead, from securing long-term contracts to ensuring project bankability. Don't wait! Watch now!World Hydrogen Week is a premier hydrogen conference organized by World Hydrogen Leaders, a part of SP Global Commodity Insights. WHW curates groundbreaking insights from industry leaders, organizes networking with key decision-makers, and showcases innovative tech and site visits!

Nordic Node, Government of Denmark, A.P Moller Mærsk, European Energy and Technip Energies share their thoughts in "Capitalising on the Nordics pivotal role in the European hydrogen economy" at World Hydrogen Week 2024 on Wednesday 2nd October 2024 at the Bella Center in Copenhagen, Denmark Join us live at World Hydrogen Week 2024 at the Bella Center in Copenhagen.

Guest Speaker - Dr Linda Yueh CBE, Adjunct Professor of Economics, London Business School speaks live at World Hydrogen Week 2024 on Tuesday 1st October 2024 at the Bella Center in Copenhagen, DenmarkWatch live as Dr Linda Yueh shares her "Analysis of the economic growth for the global economy and energy: are they forever linked?"

As the hydrogen industry makes unprecedented advancements around the world, from new policies and regulations to projects reaching FID, the hype is now far behind us. The time has come to tackle practical realities of projects on the ground and eliminate bottlenecks to system-wide deployment. Despite great progress, there’s much still to be done. Learn more at World Hydrogen Week (30 September - 4 October 2024, Bella Center, Copenhagen)

Earlier this week, Nadim Chaudhry, advisor and founder of World Hydrogen Leaders, interviewed the Program Directors for this year’s 5th annual World Hydrogen Week, which will take place from 30th September to 4th October 2024 in Copenhagen.Key findings shared during the discussion included the increasing prominence of natural hydrogen, developments in the Chinese hydrogen market, trends related to projects reaching 'Final Investment Decision' (FID), and shifts in policy and regulation.Join us at World Hydrogen Week this comprehensive hydrogen conference will feature multiple events and streams, bringing together over 3,500 industry experts in Copenhagen this Autumn. Don't miss out on the premier global hydrogen event of the year!Register here

Today's episode of Energy Evolution is all about the Advanced Clean Energy Storage project in Delta, Utah. ACES will use electrolysis to convert renewable energy into hydrogen and store it so that the otherwise intermittent resources will be dispatchable on demand from storage in large salt caverns underground. The first project will convert and store up to 100 metric tons per day of hydrogen and is expected to enter commercial-scale operations in mid-2025.Chevron recently acquired Magnum Development LLC and a majority interest in the project, which is a joint venture with Mitsubishi Power Americas.Our guests discussing the topic are Austin Knight and Michael Ducker. Knight is the vice president of hydrogen for Chevron New Energies, a division of Chevron USA Inc. Ducker is the President CEO of MHI Hydrogen Infrastructure, a wholly owned subsidiary of Mitsubishi Power Americas and a power solutions brand of Mitsubishi Heavy Industries.Subscribe to Energy Evolution to stay current on the energy transition and its implications. Veteran journalists Dan Testa and Taylor Kuykendall co-host the show, which routinely features regular correspondents Camilla Naschert and Camellia Moors

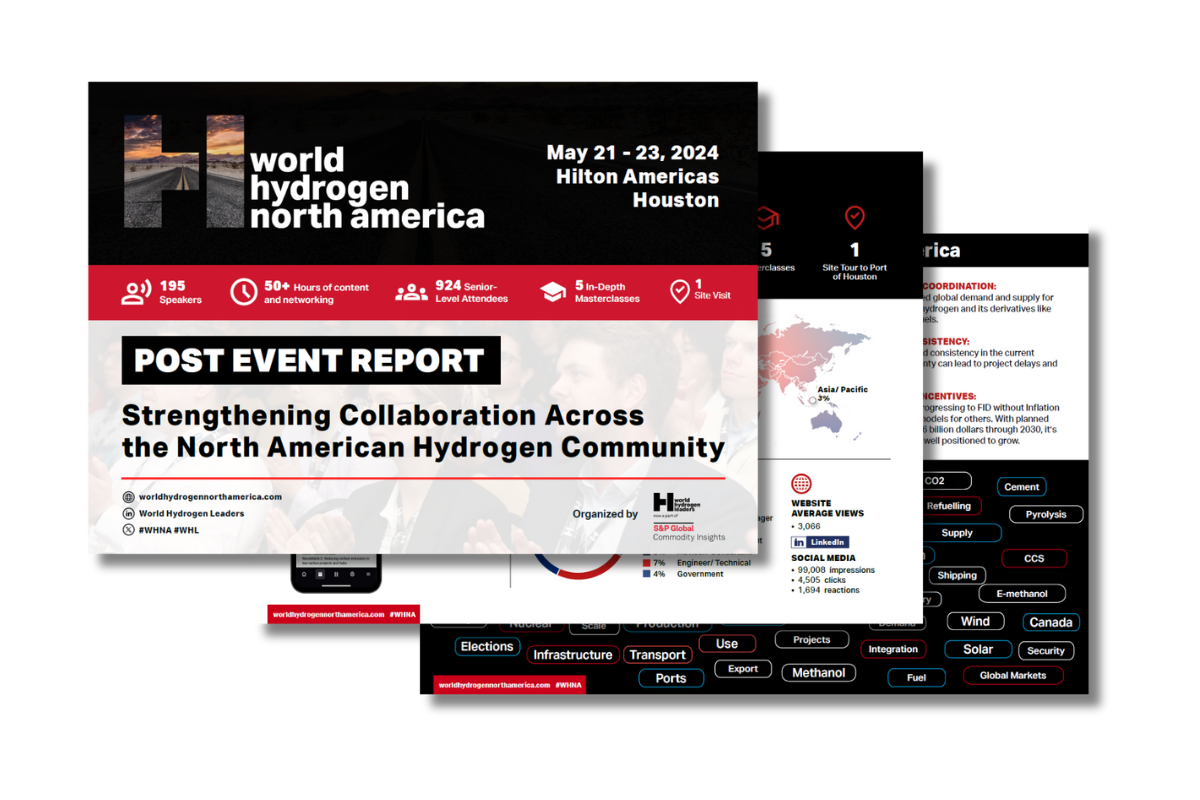

World Hydrogen North America 2024 was a resounding success, bringing together over 900 attendees from across the hydrogen value chain in Houston. With six content-rich tracks, the event offered something for everyone, covering a diverse range of topics, including tax incentives, political instability, hydrogen hubs, production, community development, tribal land, public transport and hydrogen, hard-to-abate sectors, infrastructure, finance, and risk... and more. Check out our post-event report to see a breakdown of who attended, the key takeaways from the conference debates, the 2024 expert speaker faculty, as well as our sponsors and industry partners.

World Hydrogen North America 2024 took place in Houston from May 21-23 bringing together over 900 senior level clean hydrogen professionals. The six content-rich tracks covered diverse topics including hydrogen production methods, hydrogen derivatives, end-use, finance, risk, infrastructure and export markets. The event kicked off with a popular pre-conference intelligence day, featuring an insightful session unpacking the latest developments on the Inflation Reduction Act (IRA), where the ongoing debate over 45V tax credits were discussed along with 45Q. There is still a lot of uncertainty for projects as they wait for further announcements from the Department of Energy, there is concern that the elections will hold up announcements even further. Attendees also had the opportunity to participate in interactive group discussions under Chatham House rules, providing a platform for open and candid discussions. While a wide range of topics were covered during the main two days of the event, one overriding theme emerged – policy and regulation. With the looming presidential elections in the USA, political uncertainty looms large over the country. During the keynote speech by Carol Browner, the potential implications of the election's outcome on the future of hydrogen were explored, highlighting the resilience of the industry regardless of the political landscape. Some key takeaways across the main two days include:Simple, cost-effective regulations are needed; overly complex rules could diminish tax credit effectiveness.Call for global policy and certification harmonization to enable cross-border coordination.Community engagement, workforce development, collaboration and trust-building are critical enablers.Global coordination is required to unify fragmented demand and supply of low-carbon fuels like hydrogen.Projects need policy stability and consistency to reach FID; political uncertainty breeds delays.Some major projects progressing without IRA incentives, demonstrating viability. Over $46B in direct hydrogen investments planned through 2030. Despite some stagnation in hydrogen projects this year due to increasing costs, lack of clear regulatory guidance, and difficulties defining incentives, the momentum in the industry remains strong. Attendees and speakers at World Hydrogen North America demonstrated a resolute ambition to overcome these challenges and make these projects a reality. Save the date: 4th Annual World Hydrogen North America, March 31– April 2, 2025, Houston, Texas. www.worldhydrogennorthamerica.com

Dive into an electrifying conversation with Shankari SrinivasanVice President of Energy, and Catherine RobinsonExecutive Director of GasPower, and Energy Futures at SP Global Commodity Insights. Together, they unravel the latest groundbreaking trends and pivotal strategies shaping the future of the industry, straight from the Hydrogen Markets Americas conference.This dynamic discussion is part of a series spotlighting the hottest topics from the Hydrogen Markets Americas conference, held on May 7-8 in San DiegoUSA. Don't miss out on the full series—check out the other captivating episodes through the links below!Hydrogen Markets Americas with Alan HayesHydrogen Markets Americas with Bala Suresh

When it comes to carbon, the key to understanding opportunities and risks is access to consistent, comprehensive and credible data, writes Kevin BirnCarbon intensity has emerged as a new metric of competitiveness. The interest is driven by the belief that whether through the energy transition, more carbon-intensive assets, companies or commodities could be more exposed to faster-than-expected changes in demand or face new costs from incremental climate policy.Companies and their investors are keenly interested in how they can benefit from this new potential competitive framework, as well as understanding the potential risks. Key to understanding the opportunities and risks is access to consistent, comprehensive and credible data.Companies have been responding to greater interest in these data from stakeholders and regulators with increasing levels of emissions disclosure. But inconsistencies in disclosures, and the carbon accounting frameworks that underpin them, continue to limit the comparability of these data, even when comparing within the same industry.Common sources of inconsistency go beyond scope 1 and scope 2 definitions and can also include how certain emissions are estimated and which factors are used (if they are used), how co-products are treated, and the units used to present the information, with the different units not always readily convertible and thus comparable. The absence of a consistent framework continues to limit the utility of disclosure, leading to an increasing call for greater information. The irony is that more information may only exacerbate the confusion. This challenge is widely recognized by financial companies through to large industrial emitters.At CERAWeek 2024, one of the themes that presented itself around decarbonization and carbon markets was the need for a harmonized emissions accounting framework to support greater comparability across estimates. This is an active area within S&P Global Commodity Insights, which has been sharing detailed methods behind its emissions work to ensure market participants can understand and compare against our growing array of large, standardized datasets.Data quality is another source of inconsistencies between estimates that warrants more attention. For the market to be able to incorporate carbon into business decisions, the information must be believed to be accurate or representative. A greenhouse gas (GHG) emissions estimate, or claim is often based upon a spectrum of information, from observed or metered fuel or energy use to complex models and formulas based on expected or historical performance. Given the array of information often required, it is almost inevitable that some assumptions must be made. For users of these data, it is not clear what level of assumptions are being made between estimates, and thereby affecting the reliability of the result. Given sufficiently high-quality data, estimates of high reliability can be made. Today, however, emissions estimate can exhibit a wide range of rigor. Moreover, users of these data have limited ability to distinguish the differences. This erodes the confidence in these numbers, and the utility of them.Consider the scatter plot of data above contrasting S&P Global Commodity Insights’ assessment of the quality of a number of our own upstream GHG estimates against the corresponding estimate of the carbon intensity. Most of the discussion today about carbon intensity has been one-dimensional: better versus worse or high versus low.The introduction of data quality brings in another dimension and introduces trade-offs. Obviously, highly reliable estimates of lower carbon commodities or assets are desirable in all cases (bottom left in the figure). However, if a carbon intensity estimate is low but unreliable is that still more desirable? Contrast this dilemma to the market today where there is limited ability to differentiate.If the market is to act upon GHG emissions data, it must be believed to be accurate or sufficiently representative. This requires the ability to systematically communicate and track quality. The inability to distinguish quality limits the ability for users to assign value to the relative effort between estimates.For companies reporting their GHG emissions, the ability to distinguish rigor is critical to support investments in estimation improvement, such as projects to measure and monitor methane. This is a particularly important point when the outcome of investments is uncertain and could result in upward revision of emissions.The principles of data and estimate quality are well documented throughout the GHG estimation and life-cycle analysis literature. Most of the work and literature has been focused on self-assessment to identify area of improvement. However, in today’s world the need is to be able to compare.To this end, S&P Global worked with the US Department of Energy National Energy Technology Laboratory to develop a means to communicate data quality. The result was the Data Quality Metric (DQM).The initial DQM was developed with the oil and gas sector in mind. However, the concept of the DQM has broad applicability to GHG estimation and reporting with the appropriate sectoral guidance. The Data Quality Metric was first proposed in a 2022 special report by S&P Global Commodity Insights titled "The Right Measure: A guidebook for life-cycle GHG estimation of crude oil."The DQM assesses quality along two variables – reliability and representativeness – using a five-by-five pedigree matrix. Reliability is the degree to which an estimate can be depended on to be accurate, for example, the comprehensiveness of underlying data; while representativeness refers to the degree an estimate can be expected to reflect reality or to what degree the data represents the asset or assets in question.The system can be scaled from an individual flow, through to an asset and even across a value chain. Throughout, the DQM delivers a consistent two letter grade assessment. In this way, the communication value can be consistent across companies, sectors, and even value-chains, making it easily understood.The DQM is far from a perfect solution as there are far more rigorous means to assess quality. It does, however, provide a balance between granularity and ease of communication. Over time the DQM will evolve as the rigor of estimates improve, and so will our estimation. S&P Global is currently deploying the DQM at scale against its own estimates.The aim is to provide a data quality assessment with each carbon intensity estimate. We are also seeing some traction in the market with this approach. Frameworks similar to the DQM can be found as part of the Open-Hydrogen Initiative, and the advancing US Department of Energy Greenhouse Gas Supply Chain Emissions Measurement, Monitoring, Reporting, Verification Framework.If the market is going to transact on carbon, then it needs to have a consistent framework to compare, contrast and ultimately make choices. Quality needs to be part of that framework. This article was first published in the May 2024 issue of Commodity Insights Magazine

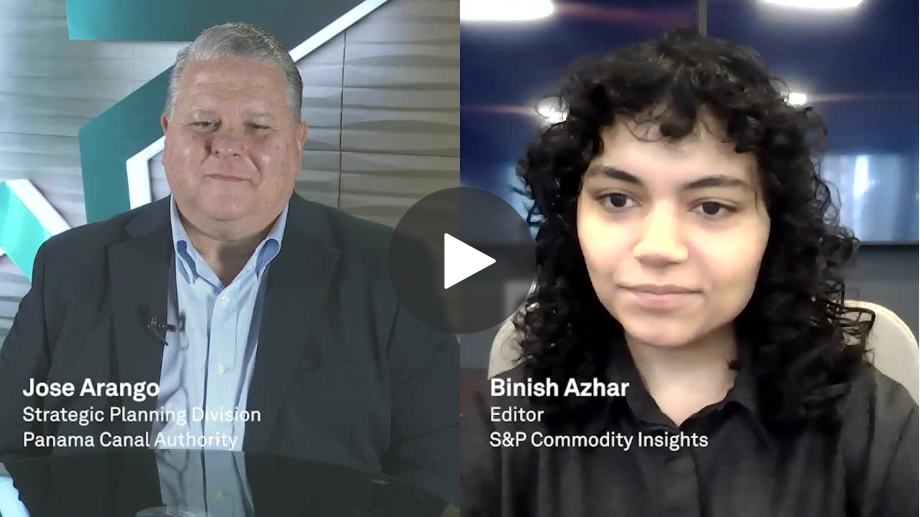

The Panama Canal Authority raised their vessel transits per day to 24 due to unexpected rain in December, and plan to keep it that way until April, the end of the country’s dry season. Jose Arango, Senior Analyst with the Strategic Planning Division of the Panama Canal Authority spoke with SP Global Commodity Insights LIVE about what’s to come, noting that the authority hopes to return to an average 36 vessel transits per day in May depending on water levels.Mr. Arango was a speaker at the Caribbean Energy Conference held in Panama from January 28-31st.

Chris Davy, deputy assistant secretary with the US Department of State’s Office of Energy Transformation, discusses the challenges to investing in the energy transition in the Caribbean and the resources developers are looking at to drive the transition away from fossil fuels.

The planned European Hydrogen Backbone pipeline system is becoming increasingly critical to the success of the continent's nascent clean hydrogen economy, with major production project developers orienting plans around the network and offtakers opening tenders seeking pipeline deliveries.The Hydrogen Backbone is expected to reach 31,500 km by 2030, with 40 concrete projects managed by the EHB's transmission system operator members set to be commissioned this decade.TSOs are anticipating a demand boom."There is no risk in my view of overbuild," Co-chair of the European Hydrogen Backbone Maria Sicilia told S&P Global Commodity Insights. "It is rather the opposite. The risk is to not build enough infrastructure to meet our decarbonization goals."Two major European industrial companies have recently announced tenders to buy clean hydrogen to decarbonize operations, in addition to the numerous bilateral offtake discussions taking place for specific projects.Oil and gas major TotalEnergies in September issued a tender to buy 500,000 mt/year of renewable hydrogen for its European refinery operations.And Thyssenkrupp is preparing a tender to purchase up to 151,000 mt/year of renewable and low-carbon hydrogen under 10-year contracts, with lower volumes starting from 2028, for pipeline delivery to its Duisburg steelworks in Germany.Meanwhile, hydrogen production project developers increasingly eye the planned pipeline infrastructure as critical to their success.HH2E secured a connection earlier in January to the European Gas Pipeline Link for the 100-MW Lubmin plant it is developing on Germany's Baltic coast. The company is working on several 100-MW plants in the country, with plans to increase to the gigawatt-scale.Also, Danish green hydrogen company Everfuel in 2023 refocused its strategy on developing large-scale production plants optimized for pipeline connection.The company highlighted a planned hydrogen pipeline between Denmark and Germany as presenting opportunities for the sector, with an anticipated start date of 2028.International pipeline trade The first phase of the Hydrogen Backbone will comprise 52% repurposed natural gas pipelines, with the rest coming from newbuild dedicated hydrogen pipes.The EHB anticipates the network expanding to 57,600 km by 2040, with 59% of this coming from converted infrastructure as the continent switches away from natural gas.Germany has committed Eur20 billion ($21.7 billion) in funds to develop its 10,000-km core hydrogen network, and the Netherlands has broken ground on a first leg of what will become a national pipeline network with cross-border connections.The EHB said its pipeline project could help lower clean hydrogen supply costs by Eur330 billion compared with a hydrogen hub model of localized regional supply and consumption.Europe's 2030 clean hydrogen plans are heavily focused on coastal Northwest Europe, while the Iberian Peninsula also has vast renewable hydrogen potential.Sicilia, who is also Strategy and Planning Director at Spanish gas transmission system operator Enagas, anticipated international pipeline hydrogen trade developing by 2030.The EHB "can create the liquidity and, as a result of cross-border trade, the internal market," Sicilia said in an interview. This would create a "pan-European market for hydrogen where you can compare costs from different regions," with substantial regional variations in price, depending on availability of renewable power resources.The pipeline network can connect low-cost production hubs with demand centers across the continent."It is going to be very different producing hydrogen from solar generation capacity in Spain or from offshore wind in the North Sea or imported from Algeria to Italy," she said.Sicilia highlighted the need for price discovery and benchmarks."Ideally, we would need to have benchmarks and reference prices so as to make the supply cost-efficient, starting with the cheapest resources."The Platts Hydrogen Price Wall shows European clean hydrogen production costs amongst the highest globally, without connections to low-cost renewables. Platts is part of S&P Global Commodity Insights.Supply and demand The EU is targeting 20 million mt/year of green hydrogen use, with half of this coming from imports. It could be a tall order, given the nascent nature of the market as it stands, and assumes sufficient offtake demand to underpin project finances, as well as sufficient availability of renewable power generation.However, the EHB has conducted a bottom-up assessment, finding some 14.7 million mt of hydrogen will be produced in Europe by 2030. This is higher than the EU's REPowerEU target, though sees imports lower.TSOs on average have around a seven-year lead time for projects, with many already underway. Final investment decisions would be needed around 2026-27 for commissioning in 2030, the EHB said.The buildout of the nascent European hydrogen economy is not without its challenges, with recent supply-chain disruptions, inflation and higher costs of capital presenting obstacles.The IEA issued a stark warning on global hydrogen developments in its Renewables 2023 report, expecting just 7% of projects targeting start dates this decade to be online by 2030 as a lack of offtakers hampers final investment decisions for project developers."We take this as a wake-up call," Sicilia said. "You can set goals, but you have to implement the policies and the funding in order to meet those goals."The EU should incentivize hydrogen demand "if we want those projects to make FID in time for 2030," she added.Just 5% of capacity targeting a start date within three years has reached FID, with many projects needing to secure an offtake in order to secure financing, S&P Global hydrogen analyst Matthew Hodgkinson said."While the commitment of public funding to revenue support schemes is encouraging for project developers, demand-side incentives are still required to facilitate uptake of hydrogen in new demand sectors," he said.

Listen now as Felipe PerezHead of Latin America Fuels and Refining Research StrategySP Global Commodity Insights sheds light on the key topics of alternative energy sources, energy security, integration towards energy transition and more from the Caribbean Energy Conference 2024.

Alex Klaessig, Senior Director, Hydrogen and Renewable Gas Forum at SP Global Commodity Insights, explores the potential impact of clean hydrogen in different sectors, from transportation and electric power to chemical feedstocks and industrial heat. Finally, Alex addresses how hydrogen developers in the US view the Inflation Reduction Act (IRA) as they await the final guidance.Conferences LIVE

The growing use of renewable energy and the phasing out of fossil fuels is creating a large flexibility gap that needs to be filled by clean technologies such as energy storage. Long-term storage technologies are critical to solar and wind power, addressing the challenge of intermittency.While lithium-ion stands as the incumbent, scaling it for extended durations proves costly. Alternative solutions poised to fill this role will need to demonstrate scalable manufacturing and large-scale deployments to meet soaring demand.In this special miniseries of the Platts Future Energy podcast, metals engagement lead Jesline Tang and energy storage analyst Susan Taylor join metals markets reporter Euan Sadden to discuss the evolving landscape of alternative long-term storage technologies, their impact on the battery sector, and how they compare to existing lithium-ion battery systems.More listening options:

MARCH | Houston, TX

Established in 1985, the World Petrochemical Conference is the premier assembly of industry leaders, global experts and government officials convening for thought-provoking dialogue and in-depth discussions around the major strategic issues facing all…